Why We Have 20 Savings Accounts & Are Opening More

Everyone needs to have money in savings. Learn how to use multiple electronic savings accounts to save more money for your family.

Do you have a savings account? How many savings accounts do you have? Would you believe it if I told you we currently have 20 savings accounts and are still adding more? We’ve been keeping multiple savings accounts for almost a decade now. It’s been 5 years since I first wrote this post and we’ve continued to open more accounts each year. (As of May 2020, we are up from 12 to 15 to 20 savings accounts.) It’s a simple thing to set up but has had a great impact on us financially. These electronic savings accounts have helped us reach many financial goals quicker than we anticipated.

Let me explain why we have so many savings accounts and how it works for our family.

This post may contain affiliate links. As an Amazon Associate, I earn from qualifying purchases. You can read more in my disclosure policy.

First of all, it’s important to know that all of our savings accounts are in one place – at Capital One 360. Capital 360 is a FDIC insured online banking program that links directly to your checking account. Yes, I’ve looked at other online accounts but so far, this account is the best one I have found.

We do have one savings account at our bank but all our other savings accounts are located at Capital One 360. For us, our electronic savings accounts serve as our digital envelopes. If you are familiar with Dave Ramsey, you’ll understand what I mean.

Having so many different savings accounts allows – and encourages – us to put money towards a specific purchase.

The one savings account that we keep at our bank serves as our personal overdraft protection from surprise bills. We keep just a little bit in there so we can move money around as necessary when it’s time to pay our bills. We’ve found that this type of slush fund works well for us.

After that, the rest of our savings accounts are at Capital One 360. We use them for several reasons.

First of all, it’s convenient that our accounts can be accessed anywhere but the online aspect keeps us in check. We can’t drive to the bank and withdraw the money we are saving. We have to plan for our purchases since it has a 3 to 5 day transfer delay to our bank. You can transfer between Capital One accounts instantaneously however.

We also like Capital One because it links to our checking account. We have set up monthly automatic transfers from our checking to a couple of our Capital One accounts. It’s nice to have savings on autopilot.

Finally, Capital One gives more interest than most accounts. I’ve seen several accounts that are at 0.01 percent interest. Capital One is currently at 3.4 percent interest with their premium savings accounts (March 2023). No, it’s not a lot compared to investments in mutual funds, but these accounts are for specific savings goals that we want to be able to access at anytime. Knowing that, it’s still good to be making a little bit in interest. I love earning free money for savings.

Now, am I suggesting that you should run out and open 20 savings accounts of your own? By no means! We started with our emergency fund and have slowly added accounts as the need arises.

What I love about having so many different savings account is that I’m no longer tempted to take from a specific savings account when it’s already earmarked for a specific goal. What goals are important to you? What do you specifically want to save for? Start by answering those questions and setting up corresponding savings accounts.

It’s also important to know that we don’t add to all of our savings accounts every month. Some we budget $100 a month for while others we add only $25 when we can. Several of our savings accounts are built solely by extra income that we earn. Some of these accounts grow when we get a tax refund. Remember, there is no certain amount that you have to save. The most important thing about saving is simply that you are saving.

So you can understand how this works for us, here is a look at all the savings accounts that we currently maintain.

Savings Account 1 – Emergency Fund

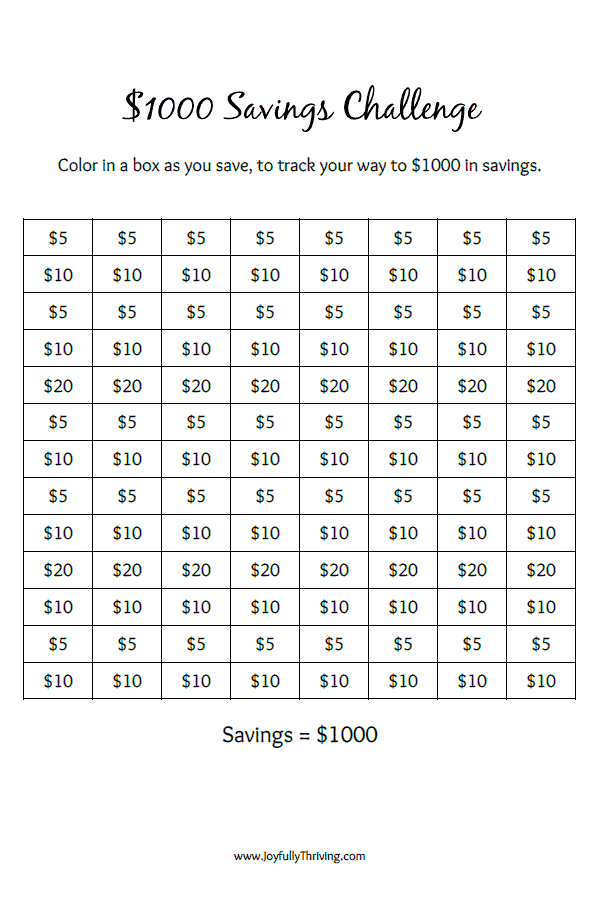

The first, largest and most important savings account we have is our emergency fund. We are fully funded with 3 months of our living expenses. We reached that goal early on our marriage and I am happy to say that we have never touched it. Still, it is amazing how an emergency fund helps me sleep better at night. I know God is in control but I also know we are called to be good stewards of all He has given us. For that reason, we plan and prepare for the emergencies that will happen at some point in time. If you don’t have anything set aside in an emergency fund, set yourself a goal of $1000. After you reach that point, increase it to 3 to 6 months of living expenses.

Savings Account 2 – Bills

The second most important savings account we have is a slush fund for our bills. We budget for our monthly bills but we all know that utility bills fluctuate. Having a cushion in this account means we are prepared for those bill overages whenever they come. This account also allows us to set aside the money for bills that are due quarterly or once a year.

Savings Account 3 – Car Repairs

We have also set up a separate savings account for car repairs. Whether it is new tires or an unexpected car repair, it is good to have money set aside for those inevitable car repair bills. We have budgeted money every month to replenishing this account because there are always car expenses for which to pay!

Savings Account 4 – New Car Fund

Along similar lines, we are also saving in our car fund account. We recently used a large portion of this account to pay cash for a new to us used mini van. It was an amazing feeling to be able to pay cash for a vehicle! Now, we are saving to replace my husband’s Tahoe which already has 260,000 miles on it. We would love to never have a car payment again so are working diligently to make this happen with this savings account.

Savings Account 5 – House Projects

We also have a savings account for house projects. Goodness knows, the list of home projects never ends! Whether it is projects like new carpet or updating light fixtures, we set money aside for any house projects that may arise. We continually add to this account because as soon as we finish one home project, there is another one on the list. Any other homeowners feel that way?

Savings Account 6 – Basement Remodel

While this could be grouped with house projects, we have a separate account for our biggest home project. We currently have a large and unfinished basement that we would like to finish someday. It will probably happen in stages over a period of years but we are adding to this account every month so the money slowly grows.

Savings Account 7 – Colts Ticket Account

My husband is a Colts season tickets holder so he has a Colts savings account. He earns money selling extra tickets so he can continue watching his beloved Colts play. Very minimal money comes out of our budget for this expense but we do have to plan ahead so he can pay for the tickets ahead of time. Your husband may not be a Colts fan but if he (or you) have a hobby that costs money, having a savings account for that expense is helpful.

Savings Account 8 – Blog Earnings

I’m excited that I have a savings account for my blog earnings. Since I started selling custom books and now that my blog is growing in size, I am actually earning money from blogging! I’m thrilled to be able to contribute to our family by blogging. I divide my blog earnings into various things over the course of the year. Some is reinvested right back into this blog, while I tithe a portion to special mission projects. I use some of my blog earnings to make an extra mortgage payment or contribute to my Roth. Until I make those payments, all my earnings sit in this account.

Savings Account 9 – Travel Fund

We have a savings account for our summer vacations and family travels. We earn free hotel nights through one credit card throughout the year but we also set aside money for other vacation expenses. Since traveling is the only way to see my spread-out family, vacations are something we choose to spend our money on.

Savings Account 10 – Christmas Gifts

We also have some money put aside in a Christmas gift account. We all know that Christmas comes every year so why not save for it year round? Most of our Christmas shopping is actually covered by free Amazon gift cards I earn throughout the year. We also shop year round for good deals on Christmas gifts that fit for our family. It’s a simple way of making this Christmas savings account stretch further.

Savings Account 11 – Someday Europe Trip

After years of adding to this account, we emptied it last summer to buy Alaska cruise tickets! We had been saving since our wedding and made the Alaskan trip happen for our 10th anniversary, thanks it large part to this savings account. Now, we are saving for our next big trip – a someday Europe trip. When we get surprise gifts, I try to tuck a little bit into this account. Maybe we’ll take a trip to Europe for our 25th anniversary?

Savings Account 12 – New Furniture / Appliances

This is an account we add to only occasionally but we do try to add to it as often as we can. When we moved into our new house 3 years ago, we bought a new upright freezer, a washer and dryer set, and a couch and love seat – all thanks to this account. We were able to pay cash for all of those big purchases because we set the money aside in this new furniture account. It makes shopping for new furnishings much easier when you know the cash is there! Of course, we still watch for sales to stretch our money further.

Savings Account 13 – Outside Projects

My husband does a lot of work outside our house and this account focus on the house projects outside. This account is where my husband saves for a replacement mower, lawn supplies, mulch and all those other sorts of outside things.

Savings Account 14 – Extra Mortgage Payment

We recently refinanced our mortgage and our payment dropped $75 a month. We are putting the difference into this savings account and making an extra payment on the principal every quarter. I ran the figures and we saved more by paying quarterly as opposed to monthly (something with compound interest that I don’t quite understand). The extra mortgage payments are automatically put in this account so we can keep paying down the principal.

Savings Account 15 – Extra Income

While my extra earnings go into blog income, any extra money my husband earns goes into this account. It simply sets the money apart until he is ready to spend it on some project or trip.

Savings Account 16 – New Roof

Our roof is over 20 years old so we have started saving for that non-glamorous but necessary replacement.

Savings Accounts 17, 18, 19 and 20 – Individual Kid Savings

As soon as our son was born, we set up a savings account for Nathan. We did this for our other children as they were born so all 4 kids now have their own savings account. Any money gifts that they receive (since all 4 kids are still quite young), we place straight in their savings fund. We have considered starting a college fund but until we finish researching and make our decision, a bit of their money is set aside.

There you have it. Those are the 20 savings accounts we currently have but we are probably not done yet. There are always new things to save for and these accounts help us reach our goals!

I believe it is a necessity for every family to have money in savings. The where and how much is up to you to determine. I hope reading how we use our different savings account has given you some encouragement to work towards your savings goals.

I’d love to know how many savings accounts you have. Also, what are you saving towards right now?

Our boys all have LCEF kids accounts because they get 3% on the first $1000 up to age 18. Also get rewards for good grades or service projects in the community, but we haven’t taken advantage of that. I am researching the next step because 1. it only goes to age 18 2. you have to be 16 to get a debit card with it and my 14 year old is earning from a summer job 3. My older 2 haven’t contributed much over the last few years because they are so close to $1000. 4. I want to put their portion of the stimulus check in savings for them. Any ideas where we could start another account for them?

This is definitely something my wife and I are wanting to do, but I haven’t processed completely how you track spending from those specific savings accounts.

For example, as we get paid we would transfer whatever money we budgeted monthly for house projects into our house projects account. If I run by the store and buy items for the house project, that money comes out of my checking or credit card. Do you balance it at the end of the month by transferring money from your house projects savings to your checking? Vacation seems simpler because you can plan for the spending and transfer prior to taking the trip.

To summarize, how do you rectify your spending (checking account/credit card) with each categorized savings account?

Thanks for your comment and question! Truly, these savings accounts have been amazing for us and I believe it can help anyone! To answer your question, we use these accounts for large projects and goals and yes, monthly transfer money into each account. Then, when we get a bill for a project or make a large purchase (say for new carpet or a car repair), we generally go ahead and put the purchase on our credit card. But, as soon as we make the purchase, we transfer the money out of the corresponding savings account into our checking so it is there and ready to pay the credit card bill. This is what works for us. We have found by doing it the day we make

the purchases, we don’t forget about it and the money is always there when we need to pay it – because we don’t carry a balance on our credit card. You could apply this same process to your checking account as well. I hope this helps explain it a bit more!

We also do this however I use my own bank since they offer free accounts there. Instead of a traditional savings account they have free checking accounts that I use as savings and only have a debit card for one of the accounts. We have accounts for the following:

1. Christmas Savers

2. Car Tags

3. Home Repairs

4. Rent (for our college kid’s house)

5. Vet

6. Vehicle Maintenance

7. Bill account

8. Hubby’s hobby

9. College Kid account (for her expenses)

10. Savings/ Emergency Fund

11. Health Savings (dr bills and pharmacy expense)

12. FSA (through my employer)

The home repair account is almost empty now as we just had to have the retaining wall on the back of our property replaced last week and my hubby is not able to do those kinds of things any more due to health so that was one expensive repair and a back breaking one for the crew that did it. Thankful I had that account set up. Now we are starting to save in it again (starting in April) to do some wood work on the house that needs to be done.

We have two accounts for medical. One through my employer and one we just save during the year. It helps when the FSA runs out. We have a lot of medical expenses as well as pharmacy expenses. It makes those months after the FSA is empty easier to bear with those “surprise bills”

We have a christmas savers account however we dont use it for christmas. It is actually designated for a large purchase two years ago it was for tires for hubby this past year it was for a tiller (so we can have a garden this year). What is left over after our planned purchase i use for christmas. We don’t go broke on christmas though.

My husband and my co-workers dont understand how we are able to just “do it” when an expense comes up but it comes from deep planning and saving and waiting until we have it to do it. We do have a couple credit cards that we use for things (and pay off from savings) to get deeper discounts and rewards on things. Also I NEVER pay full price for anything! Take for instance I have been having to replace some of my husbands clothes (due to holes and stains from his job) the local store had a 75% off sale a couple weeks ago. I bought $900 in Carhart’s for less than $300. Win for us. He has almost a whole new closet of clothes and a back up pair of work boots. We just have to wait until the store does the sale twice a year and bam!

Way to go, Rebecca! I think we are going to be setting up a new account for our medical bills too. We have an HSA through Andy’s work, and the school contributes some, but we are responsible for a large part of our high deductible every year. So far, we just put in a large lump sum when we need to, but like you, I think it would be easier on our budget and peace of mind to have that account set up. I love how you have adapted the checking accounts to make it work for you. Like you, we use credit cards to for the rewards, but always pay it off. That is an amazing deal you scored at Carharts! It is just a matter of saving and watching the sales. Love hearing from frugal savers like you with your tips and tricks. You are an encouragement to me, too!

I currently have six savings accounts set up. Two (yes I said two) emergency funds, two accounts which are to be named later, a Pennsylvania Trip account and a Special Occasions/Holidays account. Mine are divided between Chase Bank, Synchrony Bank and Capital One 360. After 32 years, I am FINALLY getting serious about saving!

Yay! Good for you, Jen! I am a firm believer that it’s never too late to start saving! 🙂 I’m glad you have some specific savings accounts set aside for different purposes. It really does make saving easier when you can see yourself reaching a goal. Thanks for stopping by!

If you’re really into budgeting…look into YNAB-you need a budget. Once you set it up, you have access to your budget in real time. If you make a purchase or pay a bill, log it in YNAB on your computer or smartphone app and it’s updated right then.

My wife started us on it a couple years ago and since then all credit cards have been paid off. We still use them for all purchases but pay them off at least twice a month.

My car will be paid off 2 years early, our boat will be paid off 8 years early.

We have an emergency fund of 6 months expenses. My next car will be paid for in cash.

I was dead set against this when she started it because I didn’t want to have to track or think about where my money went, but 2 years later I’m glad she made us do this.

Hi, Clive. Congrats on saving so well! YNAB is a great program. We did use it for a bit, but then went back to our basic pen and paper budget. You can read about that here – https://joyfullythriving.com/2015/09/simple-budget/. For now, it’s what works best for us. I’m glad YNAB has been so helpful for you! Keep up the great work saving!

I understand your reason for having so many accounts but I wondered if you knew that some banks allow you to subdivide your account balance in a single account for these purposes. We have a PNC account with online access that permits this. I make “buckets” for all these kind of savings goals, but ultimately the money is in one account and its only the online PNC software that names and divides the buckets.

That’s nice that your bank allows you to subdivide accounts. That would be simpler than multiple accounts, but since we can’t do that with our bank, this is what works for us right now. Thanks for sharing that idea, though, Rebecca!

That’s a neat idea. I was just thinking about that tonight as we were discussing our budget and trying to figure out how we are going to keep our different savings categories separate. Currently we have our savings account with our main bank and our emergency fund with LCEF. We just looked at the kids accounts with LCEF and decided we’re making that a Christmas gift for each of the boys this year. I like having their emergency fund account for us for the full 1% interest, still so much higher than most.

Now that we have a house we’ll be setting aside savings for more of an emergency fund, taxes, house projects, a car, and vacation/traveling.

Thanks, Alisha. Yes, a house does come with lots more expenses. I hope you are settling in nicely! I think we’re going to transfer most of Nathan’s money to an LCEF account as well, to take advantage of the higher interest. We’ve found it very helpful to have separate accounts so we don’t dip from one to another. Good luck setting up your accounts and working towards your savings goals.

That’s awesome…we use Capital One as well as our regular bank. I really like how you can keep opening accounts within it and label it for specific categories/needs!

I do too, Vera. It really makes it clear and simple. I’m glad to know you’re another satisfied Capital One customer! Happy savings! 🙂

Kristen, this is such a smart way to use those accounts! I have never been a fan of the envelope technique because I would constantly have change and bills flying everywhere. But this is a unique spin that I just might have to try. 😉

Thanks, Allison! I wanted to love the envelope system but just couldn’t get it to work for us. Having multiple savings accounts works for both me – and my husband! It’s so nice to be able to open our accounts and see at a glance how we are doing with our savings accounts. Capital 360 even allows you to set goals on your accounts so you can track your savings progress. Good luck, and let me know how it works for you!

Very cool! I’m going to talk to my husband about setting something like this up! It would be really helpful for us to have our savings divvied up similar to htis!

Thanks, Kate! It really is very helpful to keep everything separate. This system has worked wonderfully for us! My only regret is that we didn’t start doing this years ago! 🙂 You’ll have to let me know what you end up doing!

What a great way to set up your savings. We have two savings accounts. I have a budget binder with sheets for each item we are saving for and how much we add each month with a running tally. It works well for us. I have to take about 2 hours each payday to balance and add everything in, but your system for others who don’t want to hassle with balancing the books would work really well. Thanks for sharing your system.

Thanks, Shelly! I think everyone needs to save how it works best for them. That’s good that you have a detailed running tally system set up. It’s a great idea to track the amounts you’re transferring each payday. Thanks for sharing your system, too!

Thanks for sharing all your savings account details! We only have one savings account, and I’d like to create more, but it just keeps being pushed aside. Currently I have a spreadsheet that helps me track how much is in each of our goals categories, but I think having separate savings accounts would make it much easier to track!

You are very welcome, Charlee! That was exactly my problem. When I tried to keep everything straight in one account, it was just too confusing. Now that we have so many different accounts, it’s simple again. I only wish I had done this years ago!

I highly recommend a LCEF savings account for Nathan because the interest rate until $1000 or age 18 is so good. We just began accounts for our boys last winter and they love to get their statement each month.

That’s a great point! I just looked at their interest rate of 3.5% and will add that to our to do list! Especially, since there are the bonuses for good grades and service behavior…when Nathan gets older. My parents opened LCEF accounts for all their grandkids, but it’s time for us to do the same.